Tokenized funds have moved from slideware to shipping products, and the pace is accelerating. Readers will leave with a clear view of what “on-chain ETF layer” really means, what BNY Mellon is enabling, where the risks sit, and how to evaluate chain choices and service providers.

The timing matters: multiple live launches, improving custody, and growing on-chain RWA balances suggest a first real distribution layer is taking shape on public blockchains. The question isn’t whether tokenization works — it’s whether waiting now means ceding distribution to faster peers.

Yes — large managers are rolling out tokenized funds faster to avoid missing an emerging on-chain distribution layer, with BNY Mellon often providing the regulated backbone. Momentum is real, but not all products will find liquidity or regulatory clarity. Early movers gain operational muscle memory and investor relationships; latecomers may still benefit by copying proven templates.

- Live signals: Baillie Gifford’s UK-regulated BAGEY launched natively on Ethereum and Solana, using BNY for tokenization and wallet infrastructure (TheStreet).

- Securitize expanded its STAC CLO fund to Solana; Ethena Labs flagged a planned $250M allocation; BNY serves as custodian/sub-adviser on underlying assets (Securitize press release).

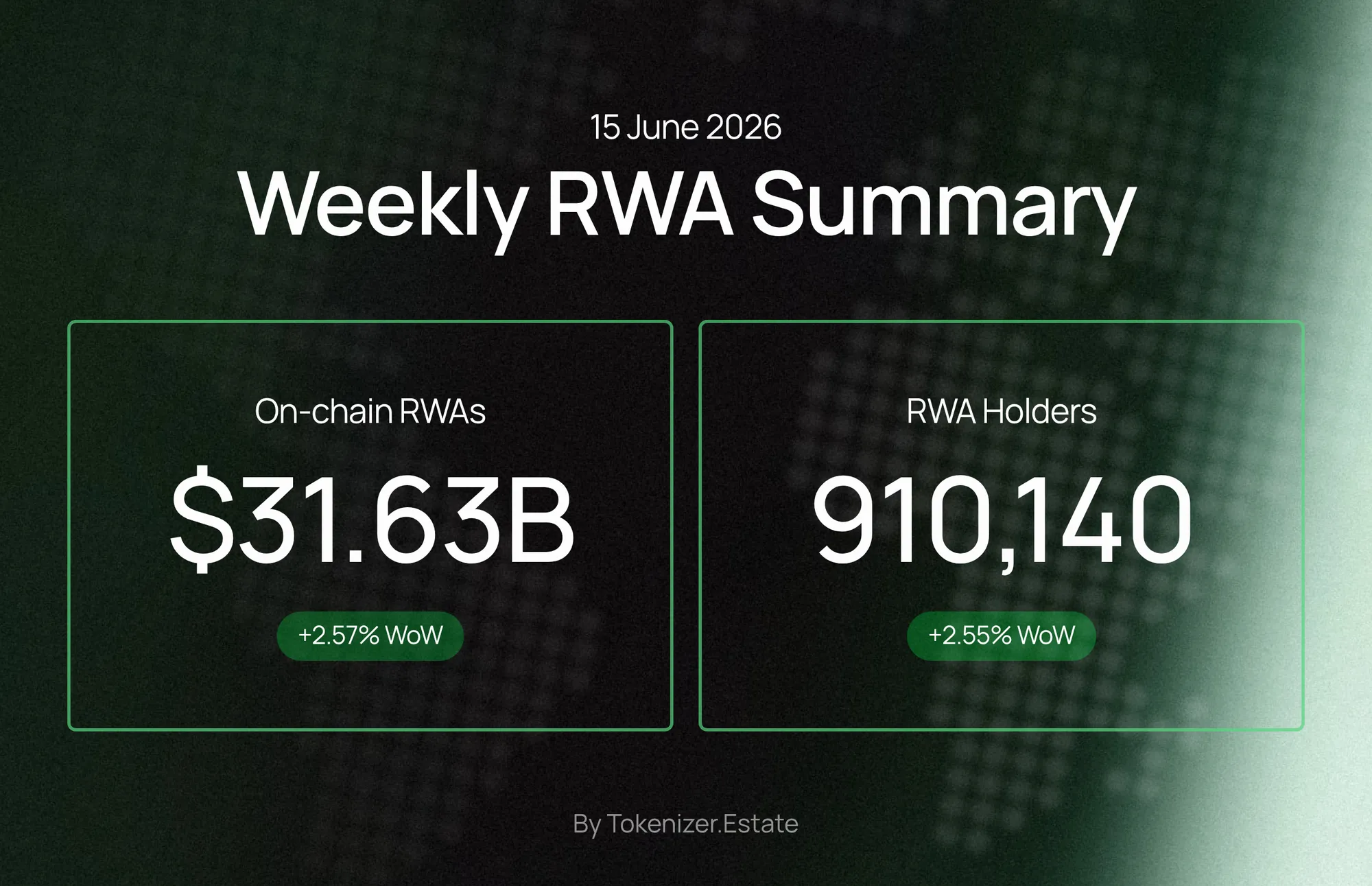

- Market backdrop: transferable RWAs rebounded to $31.63B with 910,140 asset holders (week ending 15 Jun 2026), a sign of broadening on-chain adoption (Tokenizer News).

- Scale indicator: Securitize cited $4B+ tokenized AUM as of April 2026, hinting at maturing infrastructure and pipelines (Securitize press release).

How real is the on-chain ETF layer today?

Concrete launches are replacing proofs of concept. In June 2026, Baillie Gifford introduced the Baillie Gifford Enhanced Yield Fund (BAGEY), a UK-regulated, fully native tokenized short-duration corporate bond fund on Ethereum and Solana. It targets roughly a 7% yield and relies on BNY Mellon for tokenization and wallet infrastructure (TheStreet).

Also in June, Securitize expanded its Tokenized AAA CLO Fund (STAC) to Solana, with a planned $250 million allocation from Ethena Labs. The press release highlighted BNY Mellon’s role as custodian and sub-adviser to the fund’s underlying assets (Securitize press release).

Beyond headline deals, aggregate RWA data shows a durable shift. Tokenizer News reported distributed (transferable) RWA value rebounded to $31.63 billion, with 910,140 asset holders as of the week ending 15 June 2026 (Tokenizer News). While definitions and methodologies vary across data providers, the trend line indicates real user counts and balances moving on-chain.

“On-chain ETF layer” isn’t a formal regulatory category today; it’s a market shorthand for ETF-like wrappers — tokenized funds with frequent liquidity windows, standardized disclosures, and automated compliance. Some live vehicles mimic ETF-like characteristics even if they aren’t exchange-listed under ETF rules. The route taken depends on jurisdiction, instrument, and service-provider stack.

What exactly is BNY Mellon enabling under the hood?

BNY Mellon, one of the world’s largest custodians, has emerged as a key enabler of regulated tokenized funds. In recent launches, it is positioned across several layers: custody of underlying assets, tokenization and wallet infrastructure, and operational roles that interface with transfer agents and administrators. In Securitize’s STAC expansion, BNY Mellon was named custodian and sub-adviser on the underlying assets, which is a strong signal for traditional risk committees (Securitize press release).

Practically, this looks like permissioned investor whitelists embedded in smart contracts; institutional-grade key management for issuers and investors; settlement rails that sync on-chain transactions with off-chain books; and reporting pipelines that map blockchain events into fund-accounting and compliance systems. The goal is straight-through processing without abandoning the control planes mandated by regulators.

Chain connectivity also matters. BNY Mellon-backed products are appearing on Ethereum and Solana. That multi-chain stance gives managers pricing flexibility (fees and throughput), developer depth, and optionality to meet investor preferences. It also reduces concentration risk while keeping workflows consistent across chains.

For distribution, the bank’s role as a recognized counterparty can compress internal approvals at asset managers and institutional allocators. A familiar custodian standing behind tokenized workflows shortens the perceived “trust gap” between Web3 tooling and real-money mandates.

Why move now instead of waiting for perfect regulation?

Waiting reduces headline risk, but it introduces commercial and operational risk. Distribution channels tend to ossify around early standards. If investor onboarding and KYC networks coalesce around a few tokenization stacks, late adopters may pay higher distribution rents or face lower wallet compatibility.

Operationally, teams that pilot now build skills in whitelisting, on-chain NAV syncs, and multi-chain operations. Those patterns are difficult to copy overnight. Meanwhile, live products are teaching issuers what investors actually want: liquidity windows, gas-abstracted UX, and simple tax reporting. Bypassing that feedback loop is a strategic handicap.

Momentum is also tangible. Securitize cited $4 billion+ in tokenized AUM as of April 2026, offering a proxy for the scale of pipelines and institutional interest (Securitize press release). And with BAGEY’s UK-regulated, native on-chain design spanning both Ethereum and Solana, the path to compliant tokenized vehicles no longer looks theoretical (TheStreet).

Pro tip: Treat your first launch as a “closed loop” sandbox — KYC-gated investors, known venues, strict transfer rules, and a defined redemption calendar. Nail operations and reporting before pursuing broader secondary liquidity.

Which chains make sense for tokenized funds in 2026?

Use cases are parsing along chain characteristics. Ethereum offers broad institutional recognition, deep tooling, and mature security practices, which helps with audits and governance. Solana delivers speed and low fees, which suit frequent subscriptions/redemptions and micro-denominated distributions. Many issuers now design for both, following Baillie Gifford’s dual-chain approach for BAGEY (TheStreet), while others prioritize Solana’s throughput for structured-credit flows like STAC (Securitize press release).

Chain choice should follow the product’s liquidity cadence, investor wallet habits, and compliance needs. Tokenized sovereigns and corporates that target broad institutional distribution might lean Ethereum-first; structured credit and frequent cash flows may tilt toward Solana. Either way, investors will prefer gas-abstracted UX, fiat on/off-ramps, and native corporate actions (e.g., automated coupon distributions).

- Latency and fees: Favor Solana for higher-frequency flows; Ethereum for wider ecosystem integrations.

- Compliance tooling: Ensure robust whitelisting, sanctions screening, and transfer controls exist on your chosen chain.

- Wallet support: Confirm institutional wallet providers cover your chain(s) and your specific smart-contract standards.

- Interoperability: Plan for messaging or mirrored share classes if you need cross-chain distribution without bridges.

Finally, be explicit about how you’ll handle chain outages, node diversity, and version upgrades — especially for investor servicing windows.

How do tokenized funds stack up against ETFs and private funds?

Tokenized funds are not automatically “better” — they trade different sets of trade-offs. The key distinctions show up in settlement, distribution, compliance, and programmability.

| Feature | Tokenized Fund (public chain, permissioned) | Traditional ETF (exchange-listed) | Private Fund (off-chain) |

|---|---|---|---|

| Settlement | T+0/T+1 on-chain; programmable transfer rules | T+2/T+1 via exchange/clearing | Subscription/redemption windows; bilateral |

| Distribution | KYC-gated wallets; potential 24/7 access | Brokerage accounts; market hours | Placement agents; limited investors |

| Compliance | On-chain whitelists; transfer restrictions | Exchange + transfer agent frameworks | PPM-driven; exemptions and lockups |

| Programmability | Native cash flows, automation, composable APIs | Limited automation; legacy corp actions | Manual or admin-mediated processes |

| Secondary Liquidity | ATS/permissioned venues; evolving depth | Exchange order book; robust for large ETFs | Infrequent secondaries; negotiated |

| Investor UX | Wallet-based; custody choice varies | Broker UI; familiar statements | Admin portals; bespoke reporting |

For many managers, the pitch isn’t “replace the ETF;” it’s “add a tokenized share class that broadens distribution and simplifies ops.” That framing keeps listings and tickers intact while meeting digitally native allocators where they are.

What should managers check before a tokenization pilot?

Clarity up front saves quarters of rework. Decide whether you’re creating a new on-chain vehicle or adding a tokenized share class to an existing fund. The latter often shortens approvals and leverages prior filings.

Next, pick a service stack that covers custody, token issuance, transfer agency, fund administration, and reporting. Where possible, keep vendor count low and insist on SOC audits, clear SLAs, and unambiguous liability language for smart-contract issues.

- Define eligibility: Which jurisdictions and investor types? Document wallet KYC flows end-to-end.

- Choose chain(s): Map redemption windows, fee sensitivity, and wallet support to Ethereum/Solana strengths.

- NAV integrity: Specify price sources, oracle design, valuation frequency, and off-chain reconciliation.

- Transfer rules: Encode holding periods, lockups, and sanctions controls in the token contract.

- Custody model: Decide between segregated accounts vs omnibus, and define recovery flows for lost keys.

- Secondary venues: Pre-arrange ATS listings or bilateral transfer arrangements for qualified buyers.

- Corporate actions: Automate coupon/dividend accrual and distribution; plan for cross-chain parity if multi-chain.

- Regulatory mapping: Align offering docs, KIDs, and marketing with product’s legal classification.

Finally, pilot with a capped raise and known investors. Instrument the journey: onboarding time, failed transactions, reconciliation breaks, and investor support tickets. Those metrics sell the next product internally.

Weekly RWA summary graphic (June 15, 2026): shows distributed RWA value ($31.63B) and chain breakdowns — useful to visualize how on‑chain fund and credit issuance (e.g., STAC, BAGEY) is contributing to rising RWA supply and holder counts. — Source: Tokenizer News (Tokenizer.Estate)

Where are the risks hiding — and who bears them?

Tokenized funds inherit market and credit risk from their underlying assets. Beyond that, they add new vectors: smart-contract bugs, chain halts, key-management failures, and mismatches between on-chain token states and off-chain books. Contract language must make clear who bears each risk and how remediation works.

Liquidity deserves special scrutiny. Tokenized funds can enable faster settlement, but they don’t conjure buyers. If secondary venues are thin or eligibility rules are strict, investors may face wider spreads and limited exit windows. Issuers should set expectations on liquidity profiles and redemption mechanics.

On compliance, vigilance is continuous, not a one-off. Sanctions lists change, wallets move across KYC statuses, and cross-border marketing rules evolve. Encode what you can, but maintain robust off-chain monitoring and escalation paths.

Common Mistakes

- Launching chain-first, compliance-second: Pick the jurisdiction and investor set first; the technical design should follow those constraints.

- Ignoring wallet UX: Friction in KYC, gas funding, or recovery flows will crater conversions. Abstract gas and offer clear recovery options.

- Underestimating reconciliation: On-chain transfers must reconcile with fund accounting daily. Automate event ingestion and exception handling.

- Promising liquidity you don’t control: Detail subscription/redemption windows, ATS venues, and transfer restrictions up front.

- Over-fragmenting share classes: Too many chains or classes splinter liquidity and create admin sprawl. Start narrow; expand intentionally.

- Vendor sprawl without liability clarity: Consolidate providers when possible and document who pays if contracts or nodes fail.

For continuing coverage of tokenized funds, market structure shifts, and on-chain data, visit Crypto Daily.

Frequently Asked Questions

Is an “on-chain ETF” legally the same as an ETF?

Not necessarily. “On-chain ETF” is market shorthand for ETF-like features (frequent liquidity, standardized disclosures) delivered via tokenized structures. Legal classification depends on jurisdiction and filings. Many live funds today are regulated vehicles with tokenized share classes rather than exchange-listed ETFs.

Can retail investors buy these tokenized funds?

It varies by product and jurisdiction. Many current offerings are restricted to qualified or professional investors and require KYC/AML. Retail access may expand as disclosures, platforms, and regulations mature, but eligibility rules remain product-specific.

What happens if an investor loses access to their wallet?

Institutional-grade setups often support key recovery or re-issuance via transfer agents and custodians, subject to strict identity verification and legal procedures. Confirm recovery workflows in offering docs before investing.

How do redemptions work if chains go down or congest?

Well-designed products define off-chain contingency plans: queued redemptions, alternative settlement rails, and NAV hold periods until on-chain settlement clears. Issuers should publish incident playbooks and RTO/RPO targets.

Will tokenized fund shares be usable as DeFi collateral?

Some may, within permissioned pools that respect transfer restrictions and KYC. Open DeFi integrations are limited by compliance requirements. Expect growth in walled-garden liquidity first, with carefully controlled collateral frameworks.

Are cross-chain bridges required for multi-chain distribution?

Not always. Issuers can run mirrored share classes on different chains and manage parity through issuance/redemption, avoiding third-party bridge risk. Where bridges are used, institutional policies typically require audited, battle-tested options with clear incident coverage.

How often is NAV calculated and published on-chain?

Practice varies by asset class. Many fixed-income tokenized funds calculate daily NAV off-chain and sync states to the chain via oracles or admin updates. Investors should review frequency, price sources, and reconciliation controls in documentation.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

{kind=link}