You open a chart and notice it again. Bitcoin on Coinbase is a hair cheaper than on the big offshore venues. Not a one-off. It has been like this for weeks.

Now the dashboards everyone watches are saying the same thing: the Coinbase Premium Index is negative. That is trader-speak for a persistent discount on Coinbase versus elsewhere.

So what exactly is this index, why is it below zero, and should you care?

The Big Picture: Why the Coinbase Premium Matters Now

Editor’s note: Through Q1 and Q2 2026 I kept bumping into the same pattern on our desk screens: U.S. hours felt heavy while offshore stayed bid. The Coinbase premium told that story in one number. The stretch of negative prints lined up with ETF redemptions and quieter summer books, and it matched what OTC counterparties were saying about risk being tightened stateside. It was not a straight line, but the microstructure explained a lot of the chop we saw around rebalancing windows. I do not treat the premium as a signal you trade on by itself, more like a quick x-ray before you pull the trigger. — Darnell Whitaker

The market has a shorthand for U.S. demand. People look at Coinbase spot because it sits at the center of dollar rails and regulated flows. When the Coinbase price runs hot compared with offshore, folks call it a positive premium and read it as strong U.S. bid. When it runs cold, that premium flips negative and the story changes.

In mid July 2026, that story has been one of a stubborn discount. According to CoinGlass data covered by The Block, the Coinbase Bitcoin Premium Index registered roughly -0.1025% on July 17 and had been negative for 60 straight days. Earlier in the month it printed near -0.0742% for a 50-day run of subzero readings, also reported by The Block. Glassnode shows a similar picture, with a live chart around -0.086% around the same period.

A negative Coinbase premium is not just a number, it is a read on who is setting the marginal price. Recently that price has been set away from U.S. spot, and often under U.S. pressure.

Why now? Part of the answer sits with flows. U.S. spot Bitcoin ETFs had heavy redemptions late June 2026, with about 4.4 billion dollars in June redemptions and roughly 5.4 billion in net outflows for the first half, per The Block. Those do not map one-to-one into spot prints, but they shape the tapes U.S. traders stare at every day.

What Exactly Is the Coinbase Premium Index?

At its core, the Coinbase Premium Index tracks the percentage difference between the bitcoin price on Coinbase and a reference price from other large exchanges. You can think of it as a simple spread: Coinbase price minus global price, divided by global price. Positive means Coinbase is trading richer. Negative means it is cheaper.

The short version

It is a microstructure signal. Coinbase skews toward U.S. dollars, U.S. institutions, and fiat on and off ramps. Offshore venues skew toward stablecoins, perpetuals, and a broader global retail base. Comparing them helps you guess which cohort is more aggressive at the moment.

Why Coinbase versus offshore?

Because the user bases, products, and liquidity profiles are different, the prices can diverge a bit even with robust arbitrage. That small wedge holds a lot of information about who is buying, who is selling, and how urgent they are.

How It’s Calculated and Where It Can Mislead

Most public dashboards compute a near real time premium using Coinbase spot versus a composite from offshore exchanges. The idea is straightforward, but there are quirks that matter.

Mechanics that push the spread around

- Base currency differences: USD pairs on Coinbase versus USDT or USDC pairs offshore.

- Fees and rebates: maker taker structures and VIP tiers can make one venue “stickier.”

- Latency and routing: some venues update faster, some routes are slower during volatility.

- Participant mix: ETF authorized participants, U.S. brokerages, and OTC desks tend to source on Coinbase.

- Regulatory frictions: KYC and fiat wires change who trades when and how much.

Venue contrasts at a glance

| Venue | Primary quote | Typical user mix | Products | Liquidity rhythm |

|---|---|---|---|---|

| Coinbase | USD | U.S. retail, institutions, ETF APs, OTC | Spot, limited derivatives | Strong during U.S. hours, quieter weekends |

| Binance/OKX | USDT/USDC | Global retail and pros | Spot plus deep perps and options | 24/7 follow the sun, heavier Asia hours |

| Bybit and others | USDT/USDC | Derivatives focused traders | Perps and options dominate | Vol spikes align with perp rotations |

Small structural differences add up. A 5 to 15 basis point wedge can stick around longer than you expect, especially when hedgers and ETFs are the flow on one side.

Reading a Negative Premium in Mid 2026

Let’s ground this in what the data shows right now, not a textbook.

What the tape is saying

As noted above, CoinGlass readings relayed by The Block pegged the index near -0.0742% on July 7 during a 50 day negative run, then near -0.1025% on July 17 during a record 60 day negative streak, also via The Block. Glassnode had it hovering around -0.086% around the same period. The immediate takeaway is simple. Coinbase has been a touch cheaper, consistently.

How that squares with flows

ETF behavior is part of it. June’s heavy outflows, roughly 4.4 billion dollars in redemptions and 5.4 billion in H1 net outflows for U.S. spot ETFs per The Block, tell you a lot about who is in the driver’s seat. When ETFs redeem, authorized participants may need to source or hedge inventory, often where their fiat rails are, which for many is Coinbase and connected OTC venues. That tends to lean on the U.S. spot tape.

Do not overfit the signal

Negative does not automatically mean bearish for price. Sometimes it just means the marginal U.S. flow is selling or hedging while offshore is flat or slightly bid. Other times it flips positive into strength. Context is everything.

What’s Likely Driving the Discount in 2026

There is rarely one cause. It is usually a stack of small frictions that line up.

ETF and desk mechanics

- ETF outflows trigger redemptions or hedges by authorized participants and market makers.

- Those desks source or offload BTC via Coinbase spot or OTC channels tied to U.S. banking.

- Selling or hedge pressure shows up as a slightly lower Coinbase print versus offshore composites.

Stablecoin versus fiat basis

Offshore quotes are mostly in USDT. USDT can trade at a tiny premium or discount to actual dollars in fast markets. When USDT is firm or when stablecoin perps are in rich contango, the offshore composite can sit a touch higher than a pure USD spot print.

Time zones and thin books

U.S. summer hours can be thin. A few larger orders on Coinbase can nudge the premium negative and keep it there until Asia picks up the baton. That persistence is part microstructure, part seasonality.

Risk budgets and de-leveraging

After a volatile first half, some U.S. funds tightened risk. If they reduce exposure via the most accessible rail, Coinbase ends up wearing that pressure in its prints.

How Traders Use the Signal (and When to Ignore It)

The premium is not a magic indicator. It is one tile in the mosaic. There are a few common ways to put it to work without forcing a trade.

Mean reversion spreads

Arb desks already compress these spreads, but smaller traders sometimes try light mean reversion when the premium stretches beyond its usual band. Spreads can stay stretched, so size and costs matter.

Flow confirmation

Pair the premium with ETF flow prints, CME basis, and futures funding. If ETFs are bleeding and the premium is negative while perps funding is flat to negative, that is a coherent flow story. If they disagree, be careful.

Time of day filters

Some watch for the premium to relax during Asia hours, then slip back during U.S. mornings. If you track it intraday, it can help with execution timing.

A simple checklist before you act

- Check the latest premium on a trusted dashboard and note the magnitude, not just the sign.

- Look at ETF creations or redemptions and CME basis to see if the flow picture rhymes.

- Glance at stablecoin premiums or discounts to USD, especially on fast moves.

- Account for fees, slippage, and borrow costs if you are thinking about any cross venue trade.

- Size down in thin hours, and avoid chasing the last basis point.

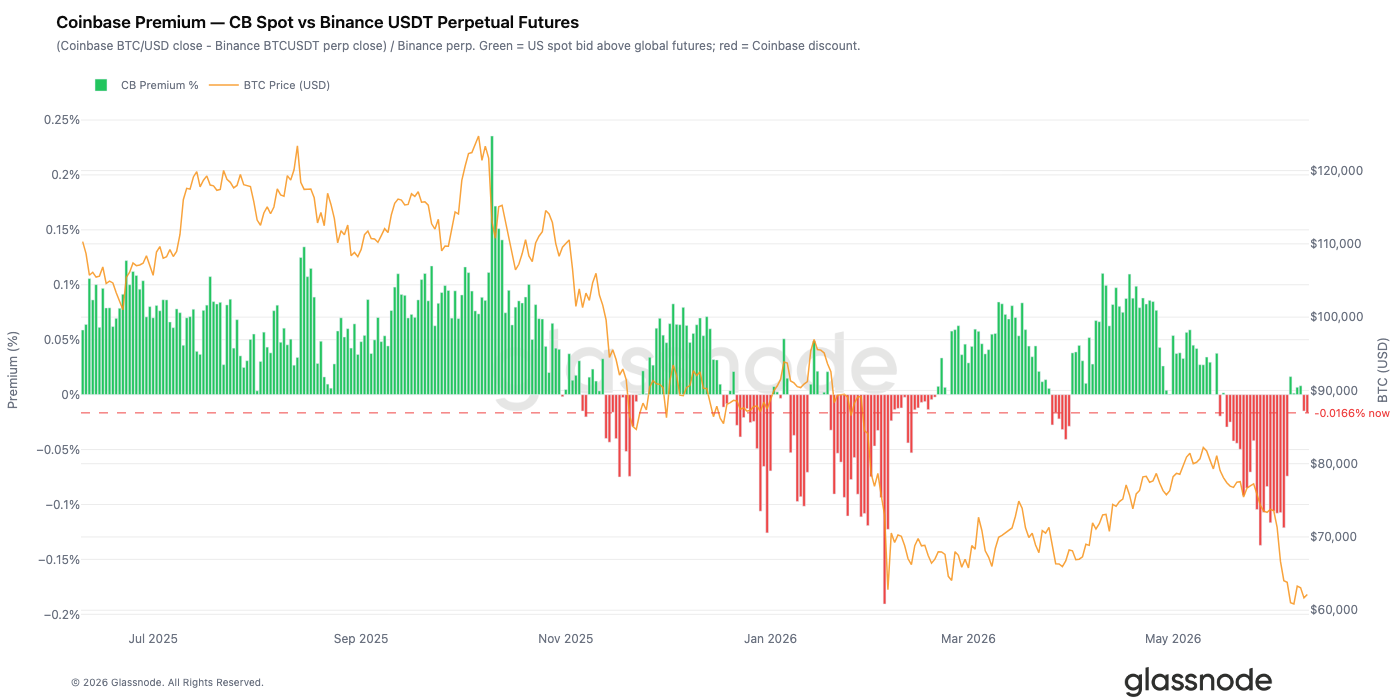

Glassnode chart “Coinbase Premium — CB Spot vs Binance USDT Perpetual Futures” showing daily premium (%) bars (green = Coinbase premium, red = Coinbase discount) alongside BTC price — visualizes the sustained negative premium since mid‑May and why analysts read U.S. spot demand as weak. — Source: Glassnode Research

What Could Flip the Premium Positive Again?

If you are wondering what changes the sign, here are the usual suspects. None are guarantees, but they are the right things to watch.

| Potential catalyst | Why it matters | Premium effect to expect |

|---|---|---|

| ETF inflow streak returns | Fresh U.S. demand routes through Coinbase and connected desks | Premium nudges positive as Coinbase bids up |

| Macro risk on | U.S. equities and rates backdrop boosts risk appetite | U.S. buying lifts USD spot versus offshore |

| USDT premium fades | Stablecoin bid normalizes after perp rotations | Offshore composite ticks lower versus USD spot |

| Liquidity programs or fee changes | Coinbase market maker incentives deepen books | Tighter spread, less persistent discounts |

| Regulatory clarity for U.S. institutions | New mandates unlock participation onshore | More onshore bid pressure |

Risks & What Could Go Wrong

- False signals: A tiny negative reading can be noise from stablecoin basis or fees, not real selling.

- Latency traps: During volatility, the composite price can lag and exaggerate the premium.

- Structural shifts: If a large venue changes fee tiers or delists pairs, the composite changes and history breaks.

- Arb constraints: Borrow limits, withdrawal queues, or custody friction can keep spreads wider than models assume.

- Regulatory shocks: A U.S. policy headline can flip flows instantly, making the last premium print stale.

- Overfitting: Building a strategy around one cross venue metric invites regime risk.

Treat the Coinbase premium as context, not a trigger. It can sharpen your read, but it should not be your only lens.

If you like to keep tabs on these moving parts without sitting on ten dashboards, the market structure coverage at Crypto Daily tracks ETF flows, on chain shifts, and exchange microstructure in one place. Worth a bookmark if this is your lane.

Frequently Asked Questions

Is a negative Coinbase premium always bearish for Bitcoin?

No. It usually points to U.S. spot being the weaker tape versus offshore at that moment. Price can still rise if offshore and derivatives flows are strong. Use it alongside funding, basis, and ETF flows.

How big does the premium need to be before it matters?

There is no hard line, but many traders only pay attention when it stretches beyond its recent range and stays there. A few basis points can be noise. Persistence across days, like the 50 to 60 day runs cited in July 2026, is more informative.

Why compare to offshore instead of CME futures?

The index is a spot versus spot comparison. CME basis is a different lens that captures futures demand from institutions. Both are useful, just different instruments and buyers.

Can stablecoin premiums distort the reading?

Yes. If USDT trades slightly rich to USD in fast markets, the offshore composite can look higher even if underlying demand is unchanged. This is why context on stablecoin flows helps.

Does ETF flow directly move Coinbase’s price?

Not directly, but it is connected. Authorized participants and market makers use U.S. rails to create or redeem ETF shares, and they often hedge or source on Coinbase or linked OTC venues. That activity can tilt the premium.

Where can I check the Coinbase Premium Index?

Public dashboards from analytics providers track it in real time. Recent readings and streaks have been reported by outlets citing CoinGlass, and the live series can also be viewed on Glassnode.

Disclaimer: This article is provided for informational purposes only. It is not offered or intended to be used as legal, tax, investment, financial, or other advice.

{kind=link}